Hi Mike,

I read One Good Trade last summer and it really turned a light on for me. Since then your weekly videos have kept me on the right path and helped me improve a little every week. I joined SMB Premium last year and then Trader90 and I’m now in DNA. It was the only logical next step. Thank you for helping me grow.

I have a question. Is Rvol (as it is used in the play book check-ups) the multiples above normal volume a stock is trading during the trade being shown? Such as an Rvol of 2 would mean the stock is trading at two times its normal volume. I can’t find the answer and I’m not sure if that’s right. If it is right then could you have a negative Rvol?

Thank you again and I look forward to our upcoming sessions.

@MikeBellafiore

I put our research intern to work for an excellent definition of relative volume and my good friend Jeff White, The Stock Bandit, had one for us…..

Relative Volume. This compares current volume to normal volume for the same time of day, and it’s displayed as a ratio. So for example, a stock trading 5 1/2 times its normal volume would have a Relative Volume display of 5.5.

Thxs Jeff!

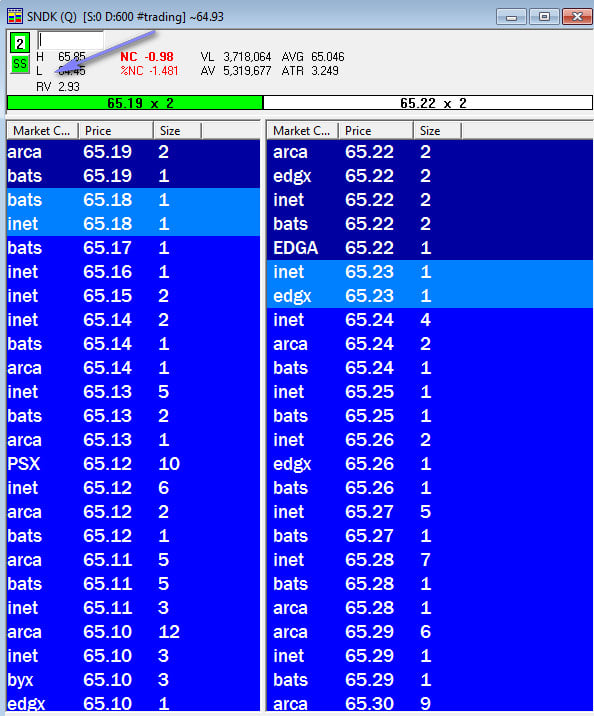

Now how do we use relative volume? We use relative volume to gauge how In Play a stock is. When I am considering trading a stock I glance at relative volume, RV on my Level 2 as the screen grab shares below.

If RVOL is less than 1 it is not In Play on this trading day and I may decide not to trade it. If RVOL is above 2 it is In Play and this is more evidence I ought to be in the name. When stocks are *very* In Play you can see an RVOL of 5 and above. The higher the RVOL the more In Play the stock is.

I also use RVOL for position sizing. If RVOL is <1 I may decide not to take a *very* large position in the name. If RVOL is >3 this may give me more confidence to take a larger position as more reward and more liquidity should be present.

I hope that helps!

Mike Bellafiore is the Co-Founder of SMB Capital and SMBU, which provides trading education in stocks, options, forex and futures. Bella is the author of One Good Trade and The PlayBook. He welcomes your trading questions at [email protected].

* no relevant positions

4 Comments on “Relative Volume (RVOL) Defined and Used”

A definition that corresponds with the actual equation used to compute it would be better.

rvol for this time of day isn’t very specific. need to know what this time of day means.

Cletus,

What Bella said is exactly correct. (I wrote the code for it so I remember!)

At any point in the day you look at how much volume the stock usually does to that point and compare today’s cumulative volume to that point. Can measure on any timeframe, but smaller resolution will be more exact (vs. juggling a lot more datapoints and memory). Also, the lookback period can vary from a week to a month or even longer, depending on what you’re trying to capture, but the concept is exactly as Bella said: the ratio of today’s volume to the average volume the stock usually does to the current time of day.

You said: “rvol for this time of day isn’t very specific. need to know what this time of day means.” It actually is very specific. “This time of day” means now… whatever time it is right now, that’s the reference point.

(A lot more volume is done in the first and last half hours of the day than is done midday, so it’s not a linear thing.)

You’re saying that “this time of day” is very specific,and of course you’re right. But without knowing whether “this time of day” means this minute, this five minute period, this hour, this whatever, it is virtually meaningless. That is what I was addressing.

Are you telling me that it is not necessary to know whether we are talking about rvol for this minute of the day, or rvol for this two hour period? Further, what is the lookback. Maybe there were earnings or a big event in the last few days that would skew this rvol tremendously.

It doesn’t seem to me to be asking too much to simply know the time period in minutes and the number of days lookback to get a much better handle on what rvol means than just to say “this time of day”.

>Are you telling me that it is not necessary to know whether we are

talking about rvol for this minute of the day, or rvol for this two hour

period? Further, what is the lookback. Maybe there were earnings or a

big event in the last few days that would skew this rvol tremendously.

I addressed both of these questions before. As I write this, it is 14:45:15 EDT. The stock market opened at 9:30:00 EDT. The total volume any stock has done today is from the open print (which, by the way, probably was not right at 9:30:00, so we use the primary exchange open) to now. Your question about time period in minutes is not relevant. Simply compare the total volume now (today) to the average of that measure at the same point on previous days.

Lookback is arbitrary. It does not matter. I can make an argument for 3 months (to capture the last earnings) or for a week (to better reflect current conditions). Default to a month if you want a place to start.

You’re making this harder than it is, and the concept is far more important than the details. There’s no secret sauce or magic formula–the concept, as Bella outlined clearly in the original post, is what matters.